英语原文共 9 页,剩余内容已隐藏,支付完成后下载完整资料

|

题目 |

Environmental performance evaluation and strategy management using balanced scorecard |

|

作者 |

Yu-Lung Hsu · Chun-Chu Liu |

|

刊名 |

Environ Monit Assess (2010) 170:599–607 |

|

来源数据库 |

Elsevier Journal |

|

原始语种摘要 |

Recently, environmental protection and regulations such as WEEE, ELV, and RoHS are rapidly emerging as an important issue for business to consider. The trend of swinging from end-of-pipe control to product design, green innovation, and even the establishment of image or brand has affected corporations in almost every corner in the world, and enlarged to the all modern global production network. Corporations must take proactive environmental strategies to response the challenges. This study adopts balanced scorecard structure and aim at automobile industries to understand the relationships of internal and external, financial and non-financial, and outcome and driving factors. Further relying on these relationships to draw the “map of environment strategy” to probe and understand the feasibility of environmental performance evaluation and environmental strategy control. |

|

关键词 |

Balanced scorecard;Environmental performance evaluation;Environmental strategy management |

|

原始语种正文 节选 |

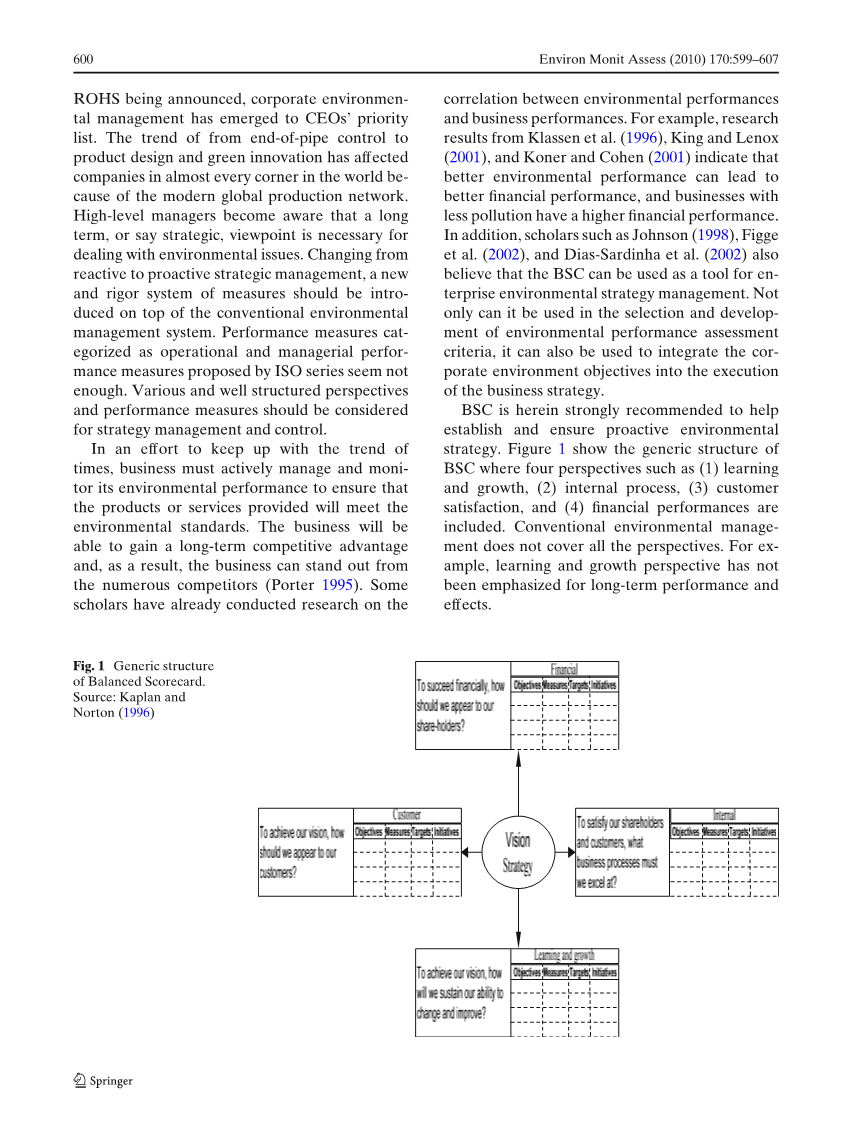

Since Kaplan and Norton (1996) proposed “balanced scorecard” (BSC) structure, many corporations have tried to implement it for strategy management. The main idea of BSC is to provide a structure of performance measures in different perspectives for focused and effective strategy management. The BSC measures cover many aspects such as internal and external, financial and non-financial, and driving and outcome factors aspects, showing long- and short-term measures simultaneously. The structure provides managers with a complete and effective control tool for corporate strategy realization. As BSC is getting popular and is welcomed worldwide, Kaplan and Norton published a book “Strategy Maps” recently, further presenting executive guide for strategy management. Strategy maps extend the BSC structure to draw a roadmap for strategy control and realization. In their new book, many case studies were shown to demonstrate the application of strategy map. One example of strategy map is about corporate sustainability strategy, which is another strong support for the main theme of this article. On the other hand, many companies have found that a reactive policy for dealing with increasingly challenging environmental issues is not enough. Especially, after many influential environmental regulations such as WEEE, ELV, and ROHS being announced, corporate environmental management has emerged to CEOsrsquo; priority list. The trend of from end-of-pipe control to product design and green innovation has affected companies in almost every corner in the world because of the modern global production network. High-level managers become aware that a long term, or say strategic, viewpoint is necessary for dealing with environmental issues. Changing from reactive to proactive strategic management, a new and rigor system of measures should be introduced on top of the conventional environmental management system. Performance measures categorized as operational and managerial performance measures proposed by ISO series seem not enough. Various and well-structured perspectives and performance measures should be considered for strategy management and control. In an effort to keep up with the trend of times, business must actively manage and monitor its environmental performance to ensure that the products or services provided will meet the environmental standards. The business will be able to gain a long-term competitive advantage and, as a result, the business can stand out from the numerous competitors (Porter 1995). Some scholars have already conducted research on the correlation between environmental performances and business performances. For example, research results from Klassenetal. (1996), King and Lenox (2001), and Koner and Cohen (2001) indicate that better environmental performance can lead to better financial performance, and businesses with less pollution have a higher financial performance. In addition, scholars such as Johnson (1998), Figge et al. (2002), and Dias-Sardinha et al. (2002) also believe that the BSC can be used as a tool for enterprise environmental strategy management. Not only can it be used in the selection and development of environmental performance assessment criteria, it can also be used to integrate the corporate environment objectives into the execution of the business strategy. BSC is herein strongly recommended to help establish and ensure proactive environmental strategy. Figure 1 show the generic structure of BSC where four perspectives such as (1) learning and growth, (2) internal process, (3) customer satisfaction, and (4) financial performances are included. Conventional environmental management does not cover all the perspectives. For example, learning and growth perspective has not been emphasized for long-term performance and effects. The advantages of adopting BSC in environmental strategy management include the following: 1. Provide complete performance measures and perspectives, 2. Offer tighter and effective management system and tool, 3. Take care of internal/external, financial/nonfinancial, driving/outcome KPI in a “balanced” way, 4. Implement BSC and generate synergy with other corporate strategy management. When facing upcoming environmental challenges, many companies may consider more proactive environmental strategy in the near future. We strongly recomm 剩余内容已隐藏,支付完成后下载完整资料 资料编号:[152498],资料为PDF文档或Word文档,PDF文档可免费转换为Word |